Aug. 26, 2025

7 Min read

Digital Banking

Share :

The rise of technology has made financial services more accessible to everyone. Technological advancements, a dynamic regulatory framework, and shifting consumer behaviour are the primary drivers behind this transformation. Traditional banks and FinTech companies are now joining forces to improve financial management using superior digital payments on investment platforms, mobile banking, Immediate Payment Service (IMPS), and Unified Payments Interface (UPI). With nearly 10.2 thousand active Fintech companies, India has emerged as a key player in digital finance. By 2030, the sector is projected to reach $2.1 trillion, growing at a strong 18% CAGR since 2022.

Despite India’s record-breaking economic growth, rural communities remain excluded from digital banking, such as Fintech applications. This is where Finkeda’s AePS services come as the most convenient technological solution. It relies solely on an Aadhaar number and a fingerprint to facilitate core transactions, making financial products accessible. Read on to understand how AePS enables distributors to play a critical role in providing vital financial services to marginalised communities. In addition, learn the complete process of AePS registration with Finkeda.

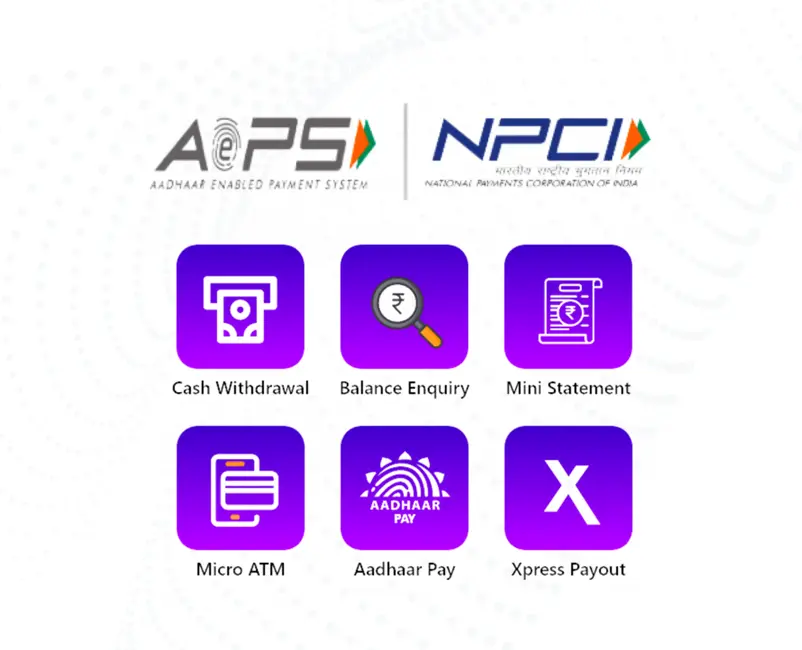

The National Payments Corporation of India (NPCI) developed the bank-driven digital payment system called AePS (Aadhaar Enabled Payment System). Customers may avail themselves of simple banking facilities such as cash withdrawal, balance check, and mini statement using their Aadhaar number and biometric authentication (fingerprint or iris scan). It is ideal for customers who reside in rural areas where it would be expensive to travel to an ATM or a bank agency. They can visit POS or micro-ATM terminals operated by local merchant representatives. In order to increase banking accessibility in remote areas, distributors are required for the onboarding and management of these merchants.

To provide banking access in underserved areas, AePS service providers frequently integrate with Public Sector Undertaking (PSU) banks, regional rural banks (RRBs), cooperative banks, and non-banking financial companies (NBFCs). AePS’ reach has been greatly increased by this integration, which makes financial services easily accessible with a single swipe. Moreover, AePS recorded 508.28 million as of June 2025.

Finkeda is offering AePS services and micro ATMs, addressing the issue of accessibility in rural India. We aim to empower local distributors by increasing their economic role through technology. Here are the major USPs and distributor benefits offered by Finkeda:

Finkeda facilitates the speedy onboarding of both distributors and their merchant networks. With minimal paperwork and plug-and-play integration, you can begin to offer services such as Aadhaar-based banking, domestic money transfers, bill payments, and add-ons like travel ticketing and insurance (as available).

All AePS transactions on the Finkeda platform are conducted through NPCI infrastructure and protected through UIDAI-verified biometrics. We follow RBI’s digital payment rules and regulatory standards for fraud mitigation.

Finkeda’s AePS portal is open 24×7 so that merchants and distributors can perform financial transactions 24×7. You can monitor transactions effortlessly through a real-time dashboard as well as track merchant performance and commission easily.

Finkeda provides instant settlement, since transactions are made within the shortest period of time. Additionally, commissions and payouts are credited into the distributor or merchant’s wallet immediately to maintain good cash flow.

Finkeda allows distributors and business owners to use minimal capital investment in order to launch services from any retail space. You get attractive commissions for every transaction, whether it’s a withdrawal, transfer, recharge, or bill payment.

Finkeda provides a scalable B2B business where distributors (also referred to as master merchants or channel partners) make money by running and growing a network of AePS-enabled retailers. After completing AePS registration, distributors obtain access to a special portal where they can onboard neighbourhood merchants, view transactions, and collect earnings. Here is how you can earn with Finkeda AePS being a distributor:

Each AEPS transaction (mini-statement, balance inquiry, cash withdrawal) executed by merchants from a distributor’s network pays the distributor a commission. Through this means, you can earn a commission on each transaction made by the service.

Volume-based bonuses are usually given to distributors after their network of retailers attains specific levels in the value of transactions or the number of transactions. For instance, Finkeda can provide enhanced payout slabs or bonus commissions as the volume increases within a month.

Distributors receive extra commissions for adding new retailers to their network. Rewards can be in the form of direct payments for every activated retailer ID or as a percentage of the retailer’s first transactions.

The central principle of earning is based on the establishment and development of a robust, active network of dealers. With even a minimum network, distributors are able to maintain and increase their monthly earnings without inventory or personnel overhead. Retained activity from retailers provides a recurring income stream, and network growth results in greater compounded earnings.

The AePS B2B model is available to individuals from diverse backgrounds, particularly those who are known to local retailers, sales merchants, or who are shop owners themselves. Make sure you meet the following eligibility criteria before going through the steps to get onboarded via the AePS portal:

After obtaining the documents listed above, go through the following step-by-step onboarding process:

Once you have been onboarded as a distributor, the next thing to do is expand your network and revenues strategically. Here’s a workable method of expanding your business using Finkeda’s AePS ecosystem:

Start by defining your coverage area. This could be your town, district, or nearby villages. Aim to onboard 50 to 100 active retailers (merchants) in the first few months. If each retailer handles just 10–20 AePS transactions a day, your network could process 15,000+ transactions monthly, translating into recurring commissions for you.

Initial setup is key. Organise demo sessions to guide your merchants through:

This minimises service faults and improves merchant confidence from day one.

Consistency is vital for development. Remain in contact with your merchant network. You can pursue strategies, including:

For instance, existing customers can be educated on how to sell mini-statements or bill payment facilities.

Visibility leads to adoption. To make your merchants successful:

The more locals understand the convenience of Aadhaar banking, the more your merchants will be approached for service. This will increase transactions and commissions for everyone in your network.

Through Finkeda, distributors are able to empower local retailers by transforming kirana stores into mini banking centres via AePS. They fill the financial inclusion gap by bringing on board and equipping these retailers with AePS integration and biometric hardware.

As a distributor within the AePS ecosystem, it provides an opportunity to generate social value beyond monetary return. Finkeda allows distributors to earn a guaranteed income on a commission-based model. It also enables kirana stores in local areas to act as banking points in unserved markets. The two-way impact makes the opportunity more satisfying and productive.

Regardless of whether you are a kirana owner in Maharashtra or a farmer from Uttar Pradesh, Finkeda’s AePS is simplifying banking for all. As India moves towards financial inclusion, offerings like AePS are a value addition to every citizen.

Share :

Like:

1