Oct. 23, 2025

3 Min read

Digital Banking

Share :

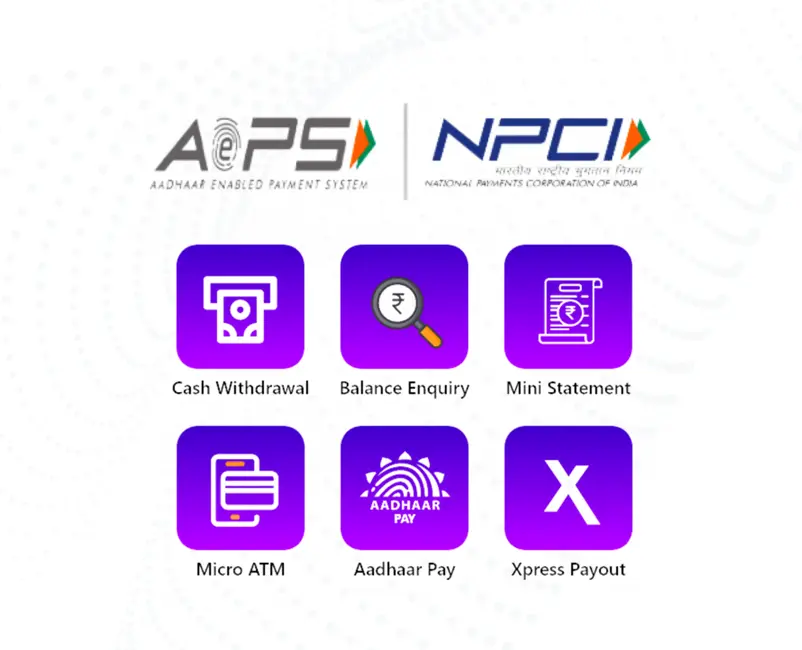

India saw over 20.01 billion Aadhaar Enabled Payment System (AePS) transactions in August 2025. This shows deep rural penetration and adoption of this banking technology across remote communities. AePS service operates as a bank-led model developed by NPCI, which allows online transactions at Micro ATM/Kiosk/mobile devices through authorized correspondents or merchants. Additionally, it provides a debt facility for rural households to boost financial inclusion in India.

AePS makes banking services available locally, creating opportunities for both customers and merchants in underserved communities. So, continue scrolling to learn what is AePS in banking and how AePS empowers rural banking and creates opportunities for earning.

In 2025, despite the government’s efforts to expand banking services in rural India, many villages still lack an ATM or a nearby branch. This hurdle in accessing banking services forces people to travel long distances. Other challenges include:

AePS debit facility lets a person withdraw cash from their Aadhaar-linked bank account using biometric authentication at a local merchant. AePS service means the merchant can use a smartphone and a fingerprint device to authenticate, and the bank can settle the debit after UIDAI verifies the biometric record. The National Payments Corporation of India (NPCI) oversees the AePS, which verifies account holders’ identities through biometric checks.

Let us discuss the step-by-step breakdown of how the system works:

With 29% of rural households still lacking easy banking access, AePS bridges the gap between unbanked populations and financial services. It places banking services at neighbourhood shops, bringing cash access and basic banking without long travel for many people in villages. Here’s how it addresses infrastructure gaps effectively:

Local shops become banking points where customers can withdraw money and check balances anytime during shop hours. This eliminates dependency on distant bank branches or ATMs that may be out of service.

Since AePS is compatible with all of India’s major banks, users can get services from any bank as long as their account is linked to Aadhaar. This flexibility solves the problem of bank-specific limitations in rural areas.

Businesses can begin providing financial services from their stores with just a smartphone, an internet connection, and a fingerprint scanner. Even in rural areas, banking infrastructure is possible due to this inexpensive setup.

Finkeda supports rural entrepreneurs through training programs and marketing materials to help them start earning commissions. Let us discuss the steps to become a certified Finkeda partner and launch an AePS service business:

AePS service has revolutionized rural banking by bringing financial services directly to village shops and eliminating the need for distant bank visits. The system empowers rural communities through simple Aadhaar-based authentication while ensuring security through biometric verification. Local merchants benefit from additional income streams while serving their communities as banking correspondents. This technology proves that banking inclusion becomes possible when services adapt to meet people where they live and work, creating sustainable economic opportunities for rural India. So, why wait? Partner with Finkeda to start providing AePS services in your region today!

Share :

Like:

23